4 Tips for Aging Better

The other day, a good friend of mine said something that stuck with me. After spending time assisting—and arguing—with his fiercely independent but not-so-agile-90-year-old father, he had a revelation. His father never thought he’d live into his nineties, so he hadn’t exactly planned for it. Of course, that meant for this particular gentleman, aging hadn’t been a graceful glissade from middle age to senior citizenship.

For most Boomers, living into your 80s and 90s is a probability—not an exception. In fact, most financial advisors will tell you to plan your finances to age 100, reducing the chances that you will outlive your money.

Putting some things in place now will make sure your life is the way you want it to be later.

Here are four tips on aging better.

1. Talk to your family.

Boy, do we hate talking with our family members about fundamental things like money, health, and—gasp!—death. But here’s the deal: if you’re going to count on them to help you later in life, then you owe it to them to tell them now what you have in mind. Let them know what resources you have (or don’t have). Tell them where important legal documents are located. Decide who gets to make important health decisions for you, if you are no longer able. One resource to get you started is a document called “5 Wishes.” It’ll help you identify your preferences regarding medical, personal, and emotional needs when you can no longer speak for yourself.

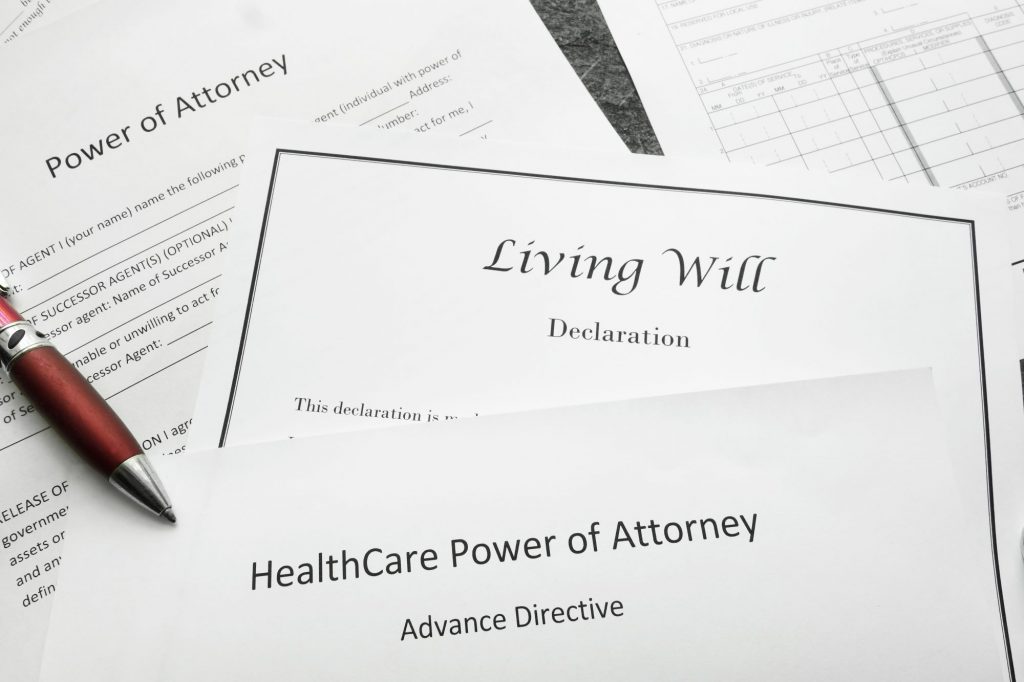

2. Get your legal documents in order.

Here are some of the legal documents that’ll make it easier for your family: a financial power of attorney; a medical power of attorney, advance directives, and a will. You can download a free copy of your state’s advance directive HERE or contact your state’s attorney general. If you have a financial planner or insurance agent, introduce them to your children or future caretakers.

3. Consider long-term care insurance.

Medicare does not pay for long-term care—except under very limited circumstances following a hospital stay. Long-term care insurance helps pay for non-medical care when you can no longer care for yourself. This type of care can range from medication management to personal grooming assistance to assisted living and nursing home care. Most plans include home care and may even help pay for modifications to your home so you can age in place. Speak with a specialist in long-term care insurance who can help you determine if it fits your needs. It’s smart to buy it when you are in your 50s or early 60s. The younger and healthier you are, the more affordable the policy will be—and the more likely you’ll be to qualify.

4. Think about where you’ll live in your “slow-go” years.

The early years of retirement are often called the “go-go years.” You’re doing all those things you couldn’t do when you were working. Great travel experiences. Making new friends. Maybe even moving to a new state for a fresh start. But if you live into your 80s and 90s, that location may no longer be right for your “going slow or no-go” years. At some point, you need to admit you will no longer be able to drive. That’s when it is time to consider transportation alternatives in the community. Think about the best place to live when you hit that stage of life. Then, do you and your family a huge favor and make the move before you have to.

It’s hard to think about a time when you can’t take care of yourself, as you have for years. But if you do, the rewards are plenty.

You’ll feel more independent and happier living in a place and way that you choose for yourself. Also, your family won’t have to worry so much about you. Now, that’s what I call “aging better.”

Laura Rossman has over 20 years of experience in health and senior care services. She currently heads up marketing and communications for iQuote by Longevity Alliance, an independent national insurance broker that helps seniors compare Medicare insurance and long-term care insurance from multiple providers.

Popular Articles About Boomer Blog

Originally published October 18, 2023